There is little doubt that in the post-pandemic world, the past nine months were the toughest phase for India’s economy as well as the stock markets. We witnessed never-like-before bullying by the US, never-like-before selling by Foreign Investors, never-like-before threat to India’s service economy due to emergence of Artificial Intelligence, short-lived but pandemic like threat to India’s supply chain during Iran war, and lastly the falling value of Indian Rupee.

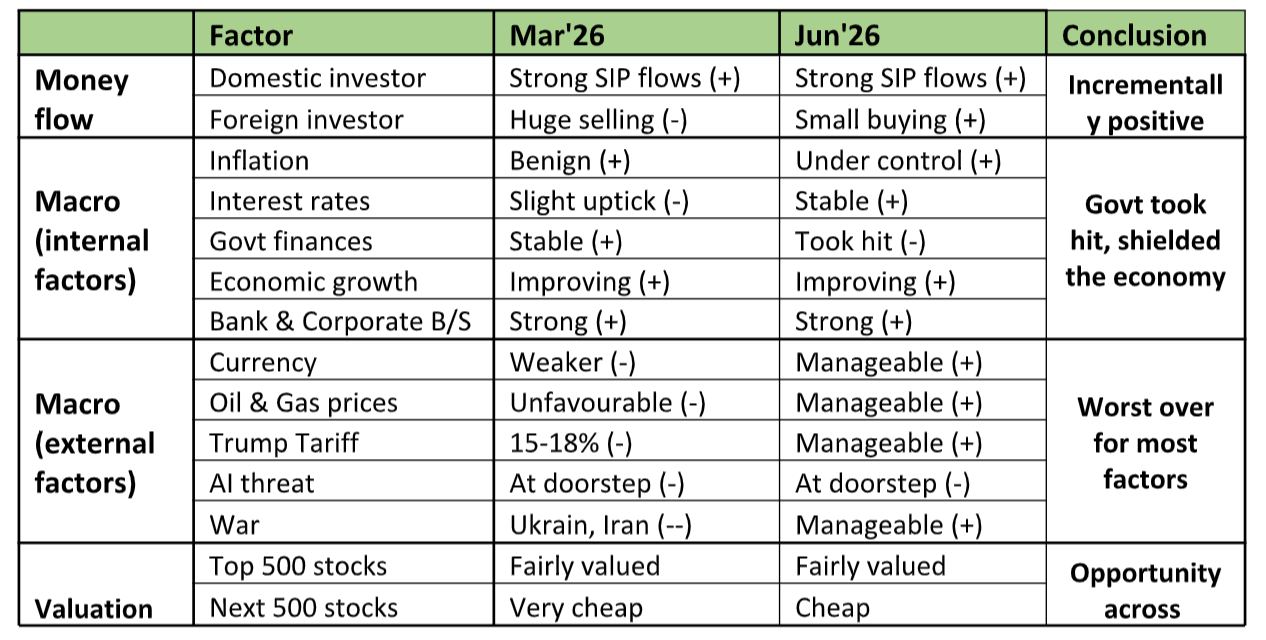

As we see the situation today, many of the above factors have started improving – some due to India’s internal efforts, some due to external factors, and some due to natural exhaustion. Whatever the reason, we can now say that the worst for India is over. The below table captures the improving situation:

Now with the benefit of hindsight, one can say that Indian government managed the wartime situation prudently. For example, taking the majority hit of high oil & gas prices on the national balance-sheet rather than passing it all to citizens & corporates. This will ensure that there won’t be big disruptions in the positive economic cycle which had started since Oct’25. Another point to note is that whenever the currency depreciates rapidly, it is the banking system and common man who pays the price (via inflation & higher interest rates). However, this time around, the government has directed RBI to bear the hedging cost on the upcoming FCNR deposit scheme, ensuring stabilization of the rupee in a non-disruptive manner.

Another factor that has turned positive for India is the stance of Foreign Investors. From being heavy sellers until May’26, they have started turning net-buyers in the month of June. Their positions are light, valuations are attractive, rupee is stabilizing, and government is promising more reforms. While the foreign investors may not rush to buy India, we can breathe a bit easy that the most intense phase of selling in India’s capital market history has come to an end.

The next 18 months – Where are the opportunities?

Given the reduced FII selling and improving macro set-up, Indian markets seem to be setting up for a broad-based rally across large, mid & small cap stocks. Of course, one must be cognizant of the fact that the “new & fast-growing” part of India is better represented by the mid & small caps rather than largecaps & megacaps. Below are some areas of long-term opportunity:

Manufacturing exports: While “Make-in-India for the world” isn’t a new theme, the recent events like signing of Free Trade Agreements with lot of smaller nations; a weaker rupee in comparison to US$ & Chinese Yuan; and rebuilding of middle-east post the war makes this theme even more attractive. Precision engineering companies operating in sectors like auto ancillary, forging, casting, stamping, machining, wire drawing, metal tube making, pump & compressor manufacturing offer multiyear growth runway.

Import substitution: Electrifying our homes, offices, factories, kitchens, transportation is the easiest way to reduce dependency on oil & gas imports. Companies that help in electricity generation / transmission / distribution, bio-energy generation, stand to benefit. Just like we came-up with plastic re-cycling mandate in 2019, India has recently introduced mandatory scrap-metal recycling.

Hi-tech investing: While the eventual winners of this AI race are still not clear, it is clear that Indian software & services companies are the losers. Another aspect where clarity is emerging is that huge capital is being committed towards building the infra needed for AI (data-centres). This is an area where opportunities are available in Indian markets as well – companies making optical fibre cables, transformers, power generators, etc and some of them are still available at reasonable value.

Domestic consumption: Sectors like Banks, NBFCs, Autos, Cement, Travel & Tourism were beaten down due to the macro shock of past few months. The fundamentals of most of these sectors are intact and they could re-bound post monsoons.

Gold & gold loans: The two biggest long-term drivers of gold prices are government debt and geopolitical stability. If we go back a little in history, the rally in gold started around the pandemic (because governments across world printed huge amounts of money). It accelerated further over 2022-25, after the US weaponised the US$ by freezing Russia’s dollar assets. Somewhere in 2025, the gold bug bit the retail investors, and we witnessed a euphoria in Jan’26.

Since then, it has corrected by 25%, partly due to war related pressures, partly due to efforts of US Fed, and mostly due to ETF selling (retail exiting). The current levels have again become attractive and the two most important long-term drivers of gold price i.e. government borrowings and geopolitical instability continue to rise every year. It is likely that central banks & smart money may once again start nibbling.

In India, we have a unique way to play gold via NBFCs that lend against gold. They have a natural tailwind of gold price and now the regulator & government also have a favourable view of the sector. As such, gold loan NBFCs also present good long-term opportunity.

Trivia – Bubbles & the return of meme stocks!

Most of us remember the GameStop saga of 2021, when the “Robinhood crowd” caused 700% rally in share price of a virtually defunct company. We witnessed a repeat of this event, when a Chinese snack company named Liu Liu Mei (LLM) witnessed 180% rally. This stock caught attention of the “Robinhood crowd” due to the acronym “LLM” in its name, which was confused with AI related acronym “Large Language Model”. Another recent India example was the sudden uptick in stock price of Parle industries (which has nothing to do with Parle Agro, which produces Melody toffee), just because Modiji gifted the toffee to the Italian Prime Minister Meloni.

“The Robinhood crowd” is a synonym for millions of young people across the globe who have taken to high frequency trading. They have neither the skillset, nor the inclination to analyse the business prospects of the company but will trade-in or out a stock / ETF / option contract based on news flow, momentum, charts, screens, prompts, filters, etc.

Whether we like it or not, the Robinhood phenomenon is here to stay. The youth across developed & developing countries have tasted initial success in the post-pandemic rally. At the same time, they are disillusioned by the mismatch between the rising lifestyle expenses and the stagnant entry level salaries. They view this high frequency trading as a lottery ticket – small losses daily but prospect of huge gains someday. This crowd has become big enough to accelerate the pace at which bubbles are created and pricked, as can be seen from the recent wild moves in gold, silver, and stocks related to artificial intelligence (data centres, fibre optics, power transformers).

This Robinhood phenomenon also has its impact on investors like us – if our stocks catch the market fancy, they get rewarded far in excess of our initial expectation & far too quickly. On the other hand, if our stocks & themes are currently not in flavour, it makes the wait period longer despite improving fundamentals. While we continue to do our stock selection based on long term trends & business fundamentals, we have enhanced our framework for scaling-up and scaling-down our positions to capture the benefit of the periodic bubbles & burst created by the Robinhood crowd.

Many studies have shown that over a long period of time more than 90% of high frequency traders end up losing their capital. As unfortunate as this is, it is the small minority i.e. experienced trader or the long-term investor who ends up cornering disproportionate gains. Someone very eloquently put this brutal truth “stock market is a machine that transfers wealth from the impatient to the patient!”

Note: One hundred percent of this article has been written by human intelligence