It is almost twelve months since we wrote the last memo, and one cannot miss a few striking similarities between Mar’25 and Mar’26 – Indian stock markets corrected sharply between Oct2024 to Mar2025 and then again from Oct25 to Mar26. Global stocks markets were doing well then and continue to do well, with more countries like Japan & Latin America joining the party.

It was easy to rationalize the correction of Oct2024 to Mar2025 because it happened after 20 months of non-stop party. One could also rationalize the current correction of Oct2025 to Mar2026 in the wake of Trump Trade Wars & Iran War; but what makes it a little more frustrating is that there was no big build-up prior to Oct’25, global markets are still doing well, and most problems that India is currently facing are external in nature (over which India has little immediate control).

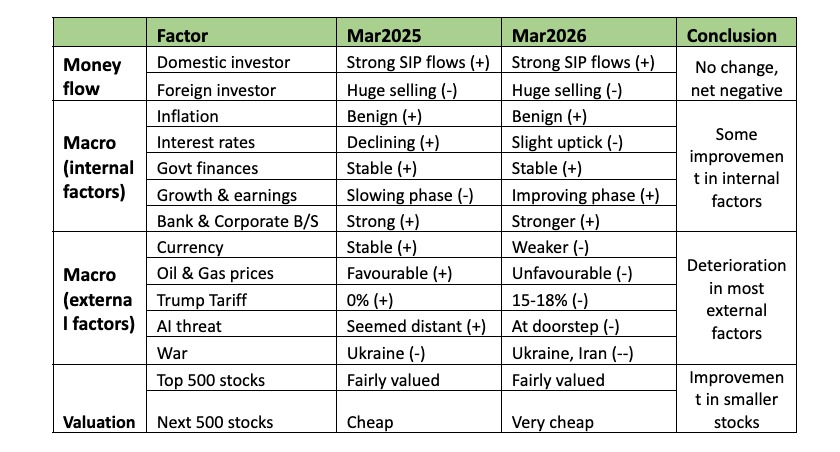

Now that we have given some vent to our frustration, we can delve deeper into the similarities & differences in the set-up for the stock markets between Mar2025 and Mar2026 to see if there are any takeaways. The below table is the summary of important factors that impact the stock market sentiment & returns.

From the table, one can roughly conclude that between Mar2025 to Mar2026, the two negatives are that money flow situation hasn’t improved and the external macro factors have deteriorated. The two positives are that there is some improvement in internal macro factors (earnings & growth) and the valuations are slightly better in smaller stocks.

What can revive the India story & the Indian markets?

If one looks at the internal situation of India, there is not much to complain – government is stable, fiscal situation is balanced, inflation is under control, there is no whiff of political or corporate scandal, there are no economic resets like demonetisation & GST, bank & corporate balance sheets are strong, earnings growth is improving. But the stable-to-improving internal situation is getting more than off-set by volatile external situation. Let us take a deeper look at some of the external problems:

FII selling: This is probably the first time in last 30 years that global markets are partying, and India has been left out. India had always received disproportionate love of FIIs due to two reasons. Firstly, we are a diversified economy & the fastest growing large economy. Secondly, most other emerging economies like China, Japan, Korea, Latin America has some or the other structural problems.

For FII, the first reason hasn’t changed. But the fortunes of other countries have started changing in the past two years and FIIs are heavily deploying their money there – China is becoming stock market friendly, Japan is reflating, Korea is benefiting from global Semiconductor, Industrial & defence boom, Latin America is making a come back due to super-cycle in metals & minerals.

Unless something goes wrong with the semiconductor boom in Korea & Taiwan, it is unlikely that FIIs will come back to India in a big way. But the silver lining is that the worst of FII selling might be over. Most FIIs are already under-weight on India, and the pace of selling could be slower from here on.

Geopolitics: Since 1990s, US has been the global superpower and US$ has been the reserve currency for global trade. Despite being just 5% of world’s population, it commands 25% of world GDP, 33% of worlds profits, and 70% of worlds market capitalization. But over the years, US abused its financial power, took on a lot of debt, and probably reached a tipping point. It can no longer bear the expenses of global policing & maintain the world order. As a result, US policy has changed towards solely looking at its own interest, even at the expense of its partners (tariffs, wars, MAGA).

This is an irreversible trend, which will continue even after Trump’s presidency. Most countries realise this and have started diversifying away from US$ (towards gold & other currencies). They have also started re-building their own defence capabilities and diversifying their own supply chains. Geopolitics will remain volatile for a few years, till the new world order is established. For investors, owning some gold & commodity linked stocks act as protection against currency dislocations.

India exports many things to the US and has been caught in this geopolitical crossfire. India is trying hard to deepen relationships with many other countries, which could open us opportunities for sectors like defence, textiles, and auto components.

AI impact: The negative scenario for India is – we have ~50 lac white collared families who collectively earn ~$150bn annually and spend it on housing, cars, education, travel, entertainment, and investment contributing to ~$600bn in GDP (15% of total). The positive scenario is that there will be huge spike in entrepreneurship – AI will enable every individual to have their own app or software, improve productivity, and increase the scope of their business activity.

We have seen that Zomato enabled thousands of new restaurants, Meesho is enabling millions of new small sellers, Insta/Youtube are birthing thousands of new content creators, Self-trading platforms have given market & data access to crores of new investors! Every path-breaking innovation destroys old jobs, creates new ones, increases productivity, and prosperity. This is because human desire is infinite – if we have free time, we will find an activity to fill it.

To us, it seems that AI will follow a similar path i.e. create more than what it destroys. Also, if AI ends up destroying everything, how will the AI companies earn a return on their huge investment? For investors, being invested in companies that have a moat in the physical world is the easiest way to navigate the current uncertainty.

Energy prices: India still has a large dependency on oil & gas (though reducing ever year). There is enough oil & gas in the world and there is no long-term worry here. The only risk is if the war in Iran & Middle East gets prolonged and prices remain high for longer.

What should an investor do in such times?

During the years of forest exile, the Pandavas came across a mysterious pond, guarded by a Yaksha (nature spirit). In the long conversation that followed between them, some wise words came from Yudhistir (the eldest brother and the prince in exile):

- What makes a person wise (Brahmin) – It is neither birth nor knowledge. It is the character shown in tough times. A scholar is no better than a fool, if he is a slave to his passions.

- Who is truly happy – A person who is in good health, has no debt, and is not forced to stay away from his home.

As investors, we may have the best knowledge & the best tools at our disposal. But if we lack wisdom & preparation to handle down phases, anxiety will get the better of us. For a long-term investor, the current market set-up is extremely favourable, where corporate earnings are improving but stock prices are subdued due to multiple external factors. It is highly likely that there will be good rewards two year down the lane.

Review your asset allocation: While stocks deliver the highest long-term returns, they also give the highest anxiety. If you are over-invested in stocks and always anxious, it may be prudent to relook at your asset allocation (and re-balance when the market recovers). If you are under-invested, this is your chance to increase allocation. A balanced mix of stocks, bonds, gold, and real estate goes a long way in reducing the financial anxiety.

Review your stock & MF portfolio: If you are a do-it-yourself investor, chances are that over the past few years, many stocks & mutual fund schemes would have entered your portfolio. Not only does it become difficult to track the huge numbers, but also the probability of outperformance significantly goes down. If doing it yourself is consuming a lot of bandwidth and creating anxiety, it may be worthwhile to hire a professional.

Review the themes that you own: Every change in macro set-up brings in new winners & losers. Till the market has good grip on AI led disruption, sectors like software, digital technology, discretionary consumption (real estate, travel, fashion, luxury) can remain subdued. On the other hand, AI and de-globalization is creating structural opportunities in sectors like the electricity sector (AI will need a lot of electricity), metals & mining, shipping, defence and manufacturing.

At Greenedge Wealth Services LLP , we continue to follow the age-old principles of asset allocation, safety and growth. Our bond portfolios continue to provide steady income, our newly re-launched mutual fund portfolio aims to generate low volatility returns from equity markets, while our equity portfolios remain geared up for the next round of wealth creation.

Trivia – Blue collar v/s White collar!

White collar job has always been the middle-class dream – study well; give a lot of importance to English language; become a lawyer or engineer or finance professional; get a desk job in A/C office; rise across ranks; keep upgrading the lifestyle. Reaching a salary bracket of 30-50lac in ten years was a given. Contrast this to the blue collared life – every technology creates disruption – salaries have only been able to catch up with inflation in huge sectors like construction, factory workers, transporters, house help, nurses, receptionist, delivery boys (2-5lac per year).

But it seems that we have reached the tipping point of this divergence. Even before the threat of AI, few things were quietly unfolding – entry level salaries for software engineers have remained around 3lac for the past 15 years, while the salaries of blue collared workers (delivery boys, drivers, full time maids) have reached similar levels. In countries like Canada, a truck driver already earns 2x more than a branch banking staff. In both the cases, it’s simply the demand supply equation that is getting balanced. We were already producing too many white collared youngsters every year even before the onset of AI – 15lac engineers, 20lac commerce graduates, and 3lac MBAs each year – most of them have limited real life skills beyond operating some tools on a computer.

These youngsters will have to adapt to the new reality – that AI will reduce entry level & mid-level desk jobs but create a lot of opportunities for micro-entrepreneurship (just like Youtube & Instagram did for social media). School & college education needs a good amount of revamp to prepare kids for micro entrepreneurship rather than desk work. Maybe it is time for the Gurukul model (focus on life skills) to replace the Macaulay system (which was designed to produce clerks).

Note: One hundred percent of this article has been written by human intelligence